European Commission publishes proposals to amend UCITS and AIFMD frameworks

Key Points to Note:

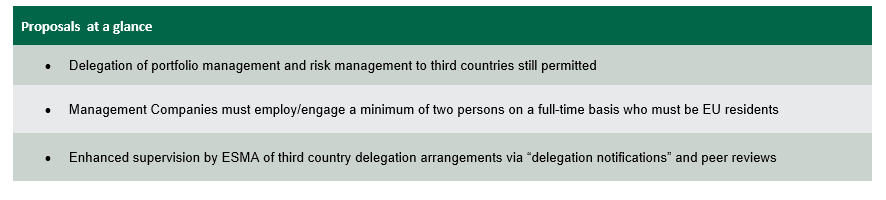

Delegation to third countries remains permissible with minimum substance requirements and enhanced supervision of third country delegation arrangements

New rules governing the use of liquidity management tools will apply to both Management Companies and National Competent Authorities

A new loan-origination framework will be introduced under AIFMD

Supervisory reporting framework for AIFMS will be revised and applied for the first time to UCITS management companies

Following a public consultation launched by it late last year, the European Commission (Commission) has now published its legislative proposal to amend both the UCITS and AIFMD frameworks (Proposal).

In this briefing, we outline some of the key proposals put forward by the Commission and potential impacts for UCITS management companies and AIFMs (Management Companies) and their funds.

DELEGATION

The Commission has noted in its Impact Assessment which was published alongside the Proposal that “a fundamental change to the AIFMD delegation rules is not necessary and the legitimate use of delegation must be preserved”, noting that the proper use of delegation arrangements have “clear benefits for EU managers and investors”.

The Commission has noted in its Impact Assessment which was published alongside the Proposal that “a fundamental change to the AIFMD delegation rules is not necessary and the legitimate use of delegation must be preserved”, noting that the proper use of delegation arrangements have “clear benefits for EU managers and investors”.

As a result, the Proposal does not introduce a wholesale revision of the delegation framework for Management Companies. Instead, it focuses on the strengthening of existing delegation rules as well as enhancing the supervision of third country delegation arrangements in order to ensure supervisory convergence across the EU and to eliminate divergent substance requirements for Management Companies located in different EU Member States. Helpfully the Commission has not proposed introducing any quantitative AUM thresholds to be considered by national competent authorities (NCA) in assessing whether or not a Management Company becomes a letterbox entity as a result of its delegation framework.

Enhancement of Requirements Applicable to New Applications involving Delegation

The Commission noted that additional measures are necessary in order to ensure that Management Companies deploy the appropriate technical and human resources to perform retained tasks where some of their functions are delegated to third parties. The clarifications proposed are intended to ensure that sufficient human resources are deployed to supervise that the delegate and core functions are retained by the relevant Management Company.

Under the Proposal, a Management Company must therefore, when applying for authorisation, describe in detail the human and technical resources it will use both to carry out its functions and to supervise its delegates including:

(a) a detailed description of their role, title and level of seniority;

(b) a description of their reporting lines and responsibilities inside and outside the Management Company;

(c) an overview of the time allocated to each responsibility; and

(d) a description of the technical and human resources that support their activities.

Minimum Substance Requirement of 2 People resident in the EU

In order to ensure a minimum, stable substance within a Management Company, the Management Company must employ at least two persons full-time or engage two persons, who are not employed by the Management Company but nevertheless are committed to conduct its business on a full-time basis and who are resident in the EU.

In an Irish context, the introduction of any such minimum substance requirement is unlikely to have any real impact on their staffing arrangements in light of the fact that the Central Bank of Ireland (Central Bank) already requires Irish Management Companies to have a minimum of three full time employees. It also expects that “a clear and convincing preponderance” of the Management Company’s Designated Persons and management roles (including key roles) be performed in Ireland.

Delegation Notifications

In order to provide ESMA and ultimately the Commission with a clearer and more reliable overview of delegation arrangements to third countries, NCAs will be required to provide ESMA with prescribed information on delegation arrangements where the Management Company delegates more portfolio management or risk management functions than it performs itself to non-EEA entities (Delegation Notifications). This Delegation Notification will require the relevant NCA to provide ESMA with information on the delegate, a description of the functions which have been retained by the relevant Management Company and which have been delegated to the third country delegate. The NCA will also be required to provide a description of any desk-based reviews and onsite inspections it has carried out on the delegation arrangement and the results of such supervisory activities.

ESMA will be tasked with drafting the technical standards which will set down the content and form of the “delegation notification” and the procedures for transmitting same to ESMA.

While it did consider granting ESMA greater powers to supervise delegation arrangements directly, the Commission has concluded that such an approach would be disproportionate and that the information gathered from Delegated Notifications should allow ESMA to assist and advise NCAs in enforcing third country delegation regimes in a consistent manner across the European Union. The obligation to approve and supervise any such delegation arrangements will therefore remain with the individual NCAs under the Proposal.

Peer Reviews

ESMA will also be required to conduct peer reviews on the supervisory practices of individual NCAs in the area of third country delegation at least every two years to assess what measures are being taken by the relevant NCA to ensure that in-scope Management Companies operating these type of delegation arrangements do not become letter-box entities.

Reporting to the Commission, Council and Parliament

Using the information which it has gathered through Delegation Notifications and peer reviews, ESMA will be required to report to the European Parliament, Council and Commission at least every two years analysing third country delegation arrangements and their compliance with the AIFMD and UCITS delegation frameworks.

Review of Delegation Framework by the Commission

The Commission will be required to carry out a specific review of the delegation frameworks under the UCITS framework 30 months after the revised delegation rules enter into force. On the AIFMD side, the Commission will carry out an overall review of the revised framework (including the new rules on delegation) five years after the new regime enters into force.

Alignment of Delegation Rules under UCITS and AIFMD frameworks

To date, the delegation rules applicable to AIFMS have been more prescriptive than the delegation rules applicable to UCITS management companies. This has been addressed under the Proposal under which UCITS management companies will be required to comply with the same delegation rules as those imposed on AIFMs. This includes imposing an obligation on UCITS management companies to justify their entire delegation structure based on objective reasons as well as giving the Commission the power to publish Level 2 measures setting down the conditions for delegation which must be completed with by UCITS management companies and the conditions under which a UCITS management company will be considered a letter-box entity which we expect will be aligned with existing AIFMD rules.

Other proposed changes to the delegation framework

The Proposal also revises the AIFMD Directive to confirm that delegates which are not authorised or registered for the purpose of asset management and subject to supervision cannot sub-delegate functions delegated to them by the AIFM.

Many Management Companies have obtained permission to not only act as AIFM or UCITS management company to funds under management but also to provide the ancillary services of individual portfolio management and other non-core services such as investment advice, safekeeping and administration of units in funds and, in the case of AIFMS, the receipt and transmission of orders. The Proposal clarifies that the delegation rules set down in the UCITS and AIFMD frameworks apply to the delegation of any such “ancillary services”.

LIQUIDITY MANAGEMENT TOOLS

Harmonisation of Liquidity Management Tools

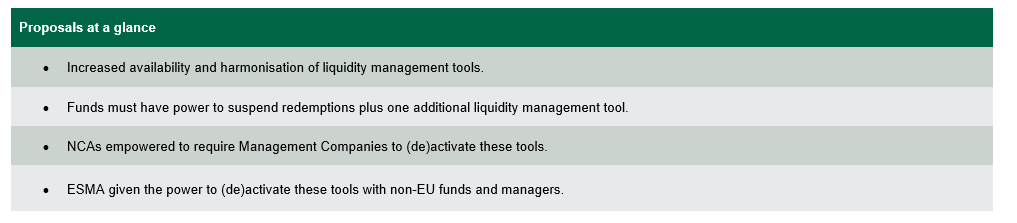

Addressing the European Systemic Risk Board’s (“ESRB”) recommendations from 20171, the Commission has proposed the harmonisation of the availability and use of liquidity management tools (“LMTs”) to UCITS funds and open-ended AIF funds.

While it acknowledges that investment funds weathered the COVID-19 storm quite well, the Commission highlights the market stress and liquidity constraints experienced during 2020 (resulting in central bank intervention) and cites the need to ensure a more efficient response by Management Companies of open-ended funds or by NCAs in market stress situations.

Concerned that the AIFMD and UCITS regimes only provide a limited harmonised solution permitting NCA to suspend redemptions in the public interest, it views harmonised LMT rules as an effective means “to protect the value of investors’ money, reduce liquidity pressure on funds and mitigate against broader systemic risk implications in situations of market-wide stress”.

Suspension and one additional LMT

The Commission proposes that Member States ensure that the LMTs set out below are available to AIFMs managing open-ended AIFs and UCITS Management Companies: ![]() Management Companies of such funds would be required to ensure they can temporarily suspend subscriptions and redemptions and would also be required to select at least one appropriate LMT from the list set above. They would also be required to implement detailed policies and procedures for the activation and deactivation of any selected LMT and disclose to investors the specific circumstances in which the relevant LMT can be used. This includes an obligation to notify the relevant NCA about activating or deactivating an LMT which is intended to allow NCAs better manage potential spill-overs of liquidity tensions into the wider market. Under the Proposal, ESMA is tasked with defining and specifying the characteristics of each of the above-mentioned LMT via regulatory technical standards.

Management Companies of such funds would be required to ensure they can temporarily suspend subscriptions and redemptions and would also be required to select at least one appropriate LMT from the list set above. They would also be required to implement detailed policies and procedures for the activation and deactivation of any selected LMT and disclose to investors the specific circumstances in which the relevant LMT can be used. This includes an obligation to notify the relevant NCA about activating or deactivating an LMT which is intended to allow NCAs better manage potential spill-overs of liquidity tensions into the wider market. Under the Proposal, ESMA is tasked with defining and specifying the characteristics of each of the above-mentioned LMT via regulatory technical standards.

Expanded regulatory powers

The Commission is proposing that NCAs be empowered to step in and require a Management Company to (de)activate an appropriate LMT, subject to prior notification to other relevant authorities, ESMA and ESRB, even in circumstances where the LMT chosen by the NCA is not provided for in the fund’s constitutive document or prospectus. Clearly concerned with macro-prudential risks, ESMA would be authorised to enable non-EU AIFMs managing open-ended AIFs to activate LMTs in exceptional circumstances.

It will be necessary to scrutinise the technical standards to understand in what circumstances NCA will be able to intervene and require a Management Company to (de)activate an LMT. However, the Proposal represents a significant expansion of regulatory powers and may cause disquiet amongst Management Companies who believe that the decision on whether to activate an LMT, and if so, which LMT should be used, should rest with the Management Company in all cases.

LOAN ORIGINATION REGIME

The Proposal set outs with some clarity the Commission’s intent to provide a harmonised EU framework for AIFMs managing AIFs in the private credit arena specifically engaging in loan origination. The Proposal identifies the need for a common set of rules to promote market integration for loan originating AIFs while at the same time ensuring a uniform level of investor transparency and protection and addressing the financial stability risks associated with the growth of this sector. In order to achieve these goals the Proposal seeks to address and implement a regime of sound processes and targeted risk management tools through a series of amendments to AIFMD. These amendments will impose some general principles on AIFMs active in the credit markets including limits on lending and requirements for loan retention which we have addressed in further detail below. It is worth noting that the Proposal expressly includes loan origination as a permitted activity in Annex 1 of AIFMD. While the Proposal notes that this is intended to legitimise lending as a legitimate activity of AIFMs, it more particularly refers to the effect of this being that AIFs could extend loans to anywhere in the EU. Whether the Commission intended that providing loan origination as a permitted activity of an AIFM to be broader in scope than just allowing for cross border lending by AIFs i.e. there might be some broader capacity for AIFMs to engage in direct lending on a cross border basis remains to be seen.

The Proposal set outs with some clarity the Commission’s intent to provide a harmonised EU framework for AIFMs managing AIFs in the private credit arena specifically engaging in loan origination. The Proposal identifies the need for a common set of rules to promote market integration for loan originating AIFs while at the same time ensuring a uniform level of investor transparency and protection and addressing the financial stability risks associated with the growth of this sector. In order to achieve these goals the Proposal seeks to address and implement a regime of sound processes and targeted risk management tools through a series of amendments to AIFMD. These amendments will impose some general principles on AIFMs active in the credit markets including limits on lending and requirements for loan retention which we have addressed in further detail below. It is worth noting that the Proposal expressly includes loan origination as a permitted activity in Annex 1 of AIFMD. While the Proposal notes that this is intended to legitimise lending as a legitimate activity of AIFMs, it more particularly refers to the effect of this being that AIFs could extend loans to anywhere in the EU. Whether the Commission intended that providing loan origination as a permitted activity of an AIFM to be broader in scope than just allowing for cross border lending by AIFs i.e. there might be some broader capacity for AIFMs to engage in direct lending on a cross border basis remains to be seen.

The general principles which it is proposed will be imposed on AIFMs managing loan originating AIFs include:

(i) Closed-ended AIF

Any AIF which engages in loan origination to “a significant extent” (articulated at 60%) must be established as a closed-ended AIF. This aspect of the Proposal is intended to address any potential for maturity mismatches that may create financial risks i.e. liquidity management risks associated with meeting investor’s expectations as regards redemption and return of capital prior to the maturity of a loan. This will not represent any change for Irish loan-originating funds which, under existing Central Bank rules must already be established as a closed-ended QIAIF.

(ii) Retention of portion of originated loans

Loan originating AIFS will be required to retain 5% of the notional value of the directly originated loans of which they have disposed. This is driven by a concern as to the “moral hazard” of originated loans being immediately sold off in the secondary market and the maintenance of the credit quality of such loans. Presumably the issue for the Commission here is that a loan originating AIF subject to the new regime should not be able to obviate the AIFMD requirements by selling off the entirety of its portfolio, however, we expect that this aspect of the proposal will be the subject of some discussion. The Proposal also clarifies that this rule does not apply to loans that such AIFs have purchased on the secondary market. It is worth noting that the CBI’s AIF Rulebook currently imposes a risk retention requirement on Irish loan-originating funds acquiring loans in the secondary market from credit institutions such that an Irish loan-origination fund must ensure that any vendor credit institution retains a material net economic interest of at least 5% of the nominal value of the loan measured at the date of origination. In light of the Proposal’s stated goal of establishing of a common set of rules for loan originating funds, it will be interesting to see whether the Central Bank will take the opportunity to revisit this requirement.

(iii) Restrictions on lending to a single borrower

In light of the concerns as to financial stability risk potentially posed by loan originating AIFs operating in the EU, it is proposed to limit the extent to which such AIFs may directly originate loans to financial institutions. In particular the proposed amendments will limit a loan originated to any single borrower to 20% of the loan origination AIF’s capital where the borrower is, in particular,

A. a credit institution

B. an insurance or reinsurance undertaking

C. an investment firm

D. a financial holding companies

E. a UCITS or an AIF

It is interesting to note however that the Proposal does provide some flexibility on these single borrower restrictions and provides (i) for a ramp-up period where permitted by the AIF’s constituent documents, (ii) disapplication when the AIF moves into harvesting mode at the end of life of the AIF and (iii) temporary suspension (12 months) where there is an additional capital raise or reduction in existing capital. In the case of any ramp-up period, the application date for the 20% restriction shall take account of the particular features and characteristics of the assets to be invested by the AIF, but shall be no later than half the life of the AIF as indicated in the AIF’s constitutive documents. However there is some discretion reserved to the relevant NCA of the AIFM to approve an extension of this time limit by one additional year. It remains to be seen the extent to which such flexibility will be afforded by relevant NCAs, the circumstances in which that might apply and the extent to which the Commission will try to harmonise parameters around such flexibility. Under existing Central Bank rules, Irish loan-originating funds are prohibited from originating loans to other funds or financial institutions (in the latter case unless there is a bone fide treasury management purpose which is ancillary to the primary objective of the relevant fund). It will be interesting to see whether the Central Bank will choose to retain this restriction notwithstanding the greater flexibility afforded under the Commission’s Proposal.

(iv) Restrictions to avoid conflicts of interests

Similar to existing rules imposed by the Central Bank on Irish loan originating QIAIFs, the Commission has also sought to address investor protection concerns related to potential conflicts of interest by prohibiting lending by a loan originating AIF to the AIFM, its staff or any entity to which it has delegated one or more management functions or the depositary.

(v) Credit Assessment and Monitoring Procedures

With the aim of ensuring the professional management of AIFs and mitigating risks with respect to financial stability, the Proposal includes requirements for AIFMs that engage in direct loan origination and the purchase of loans in the secondary market, to have effective policies, procedures and processes for the granting of loans, assessing credit risk and administering and monitoring its credit portfolio. These policies, procedures and processes will need to be in place at the establishment of the AIF but there will be an express requirement to keep those under regular review and in any event at least once a year. Again, AIFMs of Irish domiciled loan origination funds are subject to similar requirements under existing Central Bank requirements.

DEPOSITARY REGIME

Depositary Passport

While the Commission has not proposed introducing a depositary passport under this review, under the Proposal, it will be possible to appoint a depositary located in another Member State to the home Member State of the AIF, if regulated, or of the AIFM, where the AIF is not regulated subject to the depositary being obliged to co-operate with the NCA of the home Member State of the AIF as well as its own NCA. The Commission considers that this will better serve investor interests by to increasing efficiencies in the market of depositary services and reduce costs for investors. The Commission believes that the current AIFMD requirement that a depositary should be located in the same Member State as the appointing EU AIF is difficult to fulfil in smaller, more concentrated markets, where there are fewer service providers.

Central Securities Depositaries

Under the Proposal, both the AIFMD and UCITS frameworks will be revised to provide that central securities depositories (CSD) providing custody services are deemed delegates of the depositary thus bringing those CSDs into the custody chain where they are providing competing custody services. The aim of this revision is to allow for a more level playing field between custodians and ensure that depositaries have access to the information needed to carry out their duties It is also proposed in order to relieve depositaries from requirement to perform ex-ante due diligence where the custodian is a CSD because it has been sufficiently vetted when seeking to be authorised as such.

Hardwiring of EU Black list for 3rd Country Depositaries

The Commission have also proposed to effectively hardwire the EU Tax and AML Blacklist into the legislation by proposing that depositaries established in third countries should not be established in: (i) a non-cooperative jurisdictions as defined by the EU Council from a tax perspective; or (ii) a “high risk country” pursuant to Directive (EU) 2015/849 (AML Directive).

ENHANCED SUPERVISORY REPORTING REGIME/REPORTING TO INVESTORS

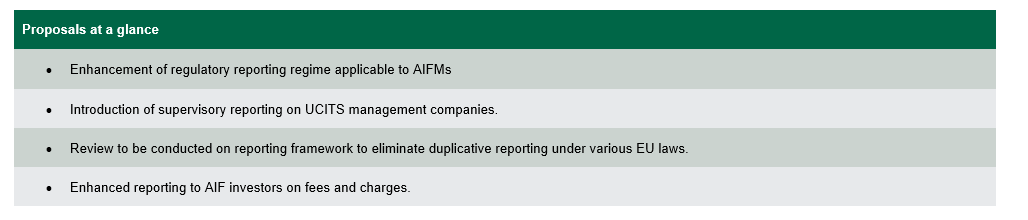

The Commission has again flagged the need to enhance the timeliness, quality and granularity of the supervisory reporting data, particularly in relation to data on leverage, liquidity profile and information on the Value at Risk (VaR) of AIFs, which is provided to NCAs in order to monitor developments in the markets and address potential risks to financial stability stemming from AIFM and AIF activities. Under proposed amendments to the existing UCITS framework, UCITS management companies will also be required for the first time to report to their NCAS on the markets and instruments in which they trade.

The Commission has again flagged the need to enhance the timeliness, quality and granularity of the supervisory reporting data, particularly in relation to data on leverage, liquidity profile and information on the Value at Risk (VaR) of AIFs, which is provided to NCAs in order to monitor developments in the markets and address potential risks to financial stability stemming from AIFM and AIF activities. Under proposed amendments to the existing UCITS framework, UCITS management companies will also be required for the first time to report to their NCAS on the markets and instruments in which they trade.

The Commission has also identified the need to remove existing reporting duplications in order to simplify and streamline current reporting obligations. Under the Proposal, a detailed study will be carried out to investigate the potential for an integrated and centralised reporting of respective supervisory and statistical data in order to reduce the administrative burdens currently experienced with duplicative reporting in place under different EU laws.

It is proposed that ESMA will be tasked with preparing a revised “Annex IV” reporting template to replace the existing template currently used by AIFMs and preparing a reporting template for use by UCITS management companies who will be required to report trade-related information to NCAs for the first time.

In line with the broader focus on costs, fees and expenses borne at investment fund level for investor protection, the Proposal also suggests imposing a reporting requirement to allow investors in an AIF to better track the investment fund’s expenses under which AIFMs should not only identify fees that will be borne by the AIFM or its affiliates but also periodically report on all fees and charges that are directly or indirectly allocated to the AIF or to any of its investments.

ANCILLARY SERVICES PROVIDED BY AIFMS

Since the introduction of the AIFMD, it has been possible for authorised AIFMs to gain additional authorisations to perform certain ancillary services under Article 6(4) of the AIFMD including individual portfolio management and non-core services (e.g. investment advice and reception and transmission of orders). Under the Proposal, AIFMs will be authorised to provide an expanded list of ancillary services including (i) the administration of benchmarks under the EU Benchmarks Regulation and (ii) the provision of credit servicing under the EU Credit Services Directive, in recognition of the increasingly important role AIFMs play within the financial system with respect to the administration of portfolios of loans and benchmarks.

Since the introduction of the AIFMD, it has been possible for authorised AIFMs to gain additional authorisations to perform certain ancillary services under Article 6(4) of the AIFMD including individual portfolio management and non-core services (e.g. investment advice and reception and transmission of orders). Under the Proposal, AIFMs will be authorised to provide an expanded list of ancillary services including (i) the administration of benchmarks under the EU Benchmarks Regulation and (ii) the provision of credit servicing under the EU Credit Services Directive, in recognition of the increasingly important role AIFMs play within the financial system with respect to the administration of portfolios of loans and benchmarks.

EU BLACKLIST COUNTRIES: IMPLICATIONS FOR NON-EU AIFS AND NON-EU AIFS

In addition to the barrier for depositaries located in jurisdictions which are designated high risk for money laundering purposes, Article 36(1) of the AIFMD (Conditions for the marketing in Member States without a passport of non-EU AIFs managed by an EU AIFM) is proposed to be amended to make it clear that non-EU AIFs which are located in jurisdictions which are identified as high risk under the AML Directive cannot be marketed within the EU. In addition, the third country where any non-EU AIF marketed within the EU is established cannot be mentioned on the revised EU list on non-cooperative jurisdictions for tax purposes and that jurisdiction must have signed an agreement with the home Member State of the authorised AIFM and with each other Member State in which the units or shares of the non-EU AIF are intended to be marketed which fully complies with the standards laid down in Article 26 of the OECD Model Tax Convention on Income and on Capital (OECD Model Convention) and ensures an effective exchange of information in tax matters, including any multilateral tax agreements.

In addition to the barrier for depositaries located in jurisdictions which are designated high risk for money laundering purposes, Article 36(1) of the AIFMD (Conditions for the marketing in Member States without a passport of non-EU AIFs managed by an EU AIFM) is proposed to be amended to make it clear that non-EU AIFs which are located in jurisdictions which are identified as high risk under the AML Directive cannot be marketed within the EU. In addition, the third country where any non-EU AIF marketed within the EU is established cannot be mentioned on the revised EU list on non-cooperative jurisdictions for tax purposes and that jurisdiction must have signed an agreement with the home Member State of the authorised AIFM and with each other Member State in which the units or shares of the non-EU AIF are intended to be marketed which fully complies with the standards laid down in Article 26 of the OECD Model Tax Convention on Income and on Capital (OECD Model Convention) and ensures an effective exchange of information in tax matters, including any multilateral tax agreements.

Similar limitations are applied to non-EU AIFMs under amendments to Article 37, Article 40 and Article 42 of the AIFMD. Consequently, non-EU AIFMs will be required to be located in jurisdictions which are not mentioned on the revised EU list on non-cooperative jurisdictions for tax purposes, which are not designated as high risk under the AML Directive and which have agreements in place with host EU member states which are compliant with the OECD Model Convention.

Consequently, such non-EU AIFMs will be required to be located in jurisdictions which are not mentioned on the revised EU list on non-cooperative jurisdictions for tax purposes, which are not designated as high risk under the AML Directive and which have agreements in place with host EU member states which are compliant with the OECD Model Convention.

NEXT STEPS

The Proposal will now be considered by both the European Parliament and the Council of Europe. Once such reviews have been independently carried out, political agreement must be reached on a finalised text. The Proposal provides for a two-year transposition timeframe within which to transpose the legislation into national law, meaning that the finalised provisions are unlikely to apply before 2025.

Should you have any questions in relation this briefing, please contact any of the authors or your usual contact in Dillon Eustace.

1 Recommendation of the European Systemic Risk Board of 7 December 2017 on liquidity and leverage risks in investment funds ESRB/2017/6, 2018/C 151/01.

DISCLAIMER: This document is for information purposes only and does not purport to represent legal advice. If you have any queries or would like further information relating to any of the above matters, please refer to the contacts above or your usual contact in Dillon Eustace.

Copyright Notice: © 2025 Dillon Eustace LLP. All rights reserved.